The FTA’s recent public clarification CTP010 explains how the UAE Corporate Tax Connected Person rules apply to salaries, bonuses, director fees, management charges and other benefits paid to owners, directors, officers and related persons, and what businesses should document during the tax period before filing, not adjusted as a year-end tax filing makeover.

—

If your business pays a salary, bonus, director fee, management charge or other benefit to an owner, a family member of an owner, director or officer, or a senior decision-maker with final strategic authority or authority to legally or contractually bind the business, the UAE Corporate Tax Connected Person rules may apply and businesses must set this correctly from the start of the tax period.

In simple terms, Connected Persons are people closely linked to the business, such as owners, directors, officers, and certain related persons, where payments to them may need extra tax support because they are not fully independent from the company.

The Federal Tax Authority (FTA) has issued Corporate Tax Public Clarification CTP010, which clarifies how the terms “director” and “officer” are interpreted when applying Article 36 of the UAE Corporate Tax Law to payments and benefits provided to Connected Persons.

CTP010 does not introduce a new tax. It explains the FTA’s interpretive position on who qualifies as a director or officer, and it has significant practical implications for owner-managed businesses, family businesses, SMEs and founder-led companies operating in the UAE.

This guide explains what CTP010 means, who it affects and what your business should do before filing its Corporate Tax Return.

Why the UAE Corporate Tax Connected Person Rules Matter

Under the UAE Corporate Tax framework, a payment or benefit provided by a Taxable Person to a Connected Person is deductible only to the extent that it reflects Market Value and is incurred wholly and exclusively for the purposes of the business.

This means a company cannot simply deduct any salary, bonus, allowance, management fee, director fee, rent or other payment on the basis that it was paid to an owner or someone associated with the business. The company must demonstrate that the payment is:

- commercially justified: the payment reflects genuine services or value;

- properly documented: supporting evidence is in place before filing; and

- not above Market Value: the amount is consistent with what independent parties would agree to under similar circumstances.

For businesses where the owners, managers and directors are often the same individuals, this requires a deliberate review of how payments are structured, classified and recorded.

Important exception: Some Taxable Persons, such as listed companies or UAE-regulated entities, may fall outside this deduction limitation. Most owner-managed SMEs should not rely on this without specific confirmation.

Who Is a Connected Person?

Under the UAE Corporate Tax Law, a Connected Person can include:

- an owner of the Taxable Person;

- a director or officer of the Taxable Person; and

- a Related Party of an owner, director or officer.

For this purpose, an “owner” means a natural person who directly or indirectly owns an ownership interest in the Taxable Person or controls the Taxable Person. A corporate shareholder may still be a Related Party, but it is not an “owner” Connected Person in the same sense. This distinction is particularly relevant for foreign-owned subsidiaries and group companies.

For an owner-managed company, the Connected Person scope can include the shareholder-manager, managing director, general manager, CEO, CFO or another senior decision-maker with final strategic authority or authority to legally or contractually bind the business. It can also extend to family members and Related Parties of those individuals, depending on the nature of the relationship and the facts of the arrangement.

Connected Persons vs. Related Parties: An Important Distinction

There is a meaningful distinction between Related Parties and Connected Persons under the Corporate Tax Law:

- Related Party rules are broader and are linked to ownership, control, family relationships, group structures and partnerships.

- Connected Person rules apply more specifically to payments and benefits made to persons closely connected to the Taxable Person, particularly owners and senior decision-makers with final strategic authority or authority to legally or contractually bind the business.

Where a person qualifies as both a Related Party and a Connected Person, CTP010 confirms that the person is treated only as a Related Party for Corporate Tax purposes. Understanding this distinction is important for how transactions are classified and disclosed in the Corporate Tax Return.

Separate rules also apply where the Taxable Person is a partner in an Unincorporated Partnership: other partners in the same Unincorporated Partnership, and their Related Parties, may also be Connected Persons under Article 36.

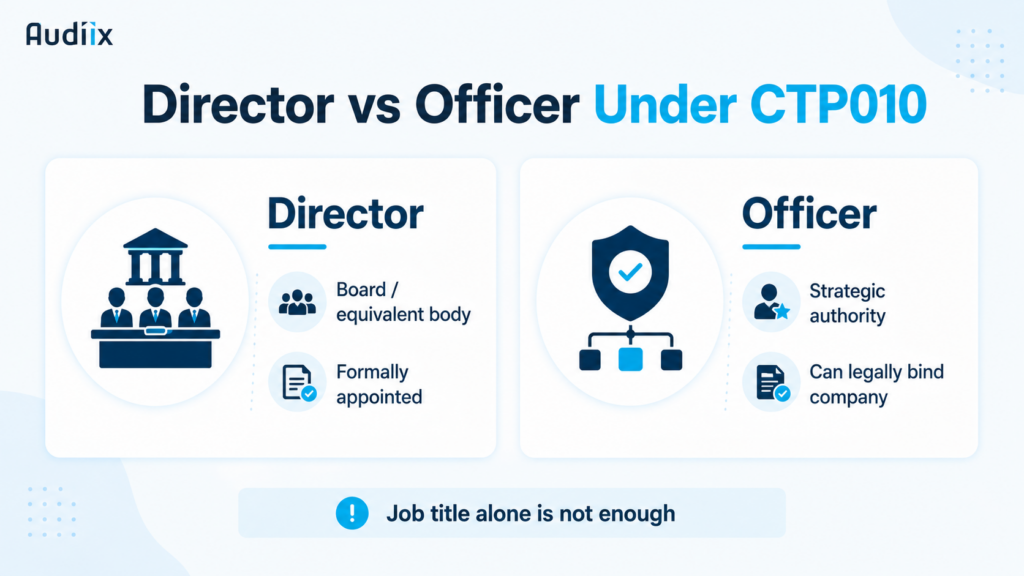

Who Is Treated as a Director for Connected Person Payments

Public Clarification CTP010 confirms that a director, for the purpose of Article 36, is a person who holds a position on the board of directors or an equivalent governing body, as determined by the law governing the Taxable Person and its constitutional documents.

This may include an executive director, non-executive director, temporary director, permanent director, alternate director or member of a board committee, provided the individual has been properly appointed to the board or equivalent body.

Job Title Alone Is Not Sufficient

A job title is not a reliable indicator. A person whose title includes the word “Director” is not automatically treated as a director under Article 36 if they do not hold a position on the board of directors or an equivalent governing body.

For example, a “Sales Director” or “Marketing Director” may not qualify as a director for Connected Person purposes if the individual has not been formally appointed to the board. That said, such a person could still be captured as an officer if they possess the requisite level of strategic authority, which is where CTP010’s clarification on officers becomes equally important.

Who Is Treated as an Officer for Connected Person Payments

CTP010 adopts a substance-based approach to the definition of officer. An officer includes a person who:

- has authority and responsibility for planning, directing and controlling the activities of the Taxable Person;

- has authority to make strategic decisions in relation to financial, operational or commercial matters; or

- has authority to enter into agreements or approve actions that legally or contractually bind the Taxable Person.

Conversely, a person is not an officer merely because they carry out operational tasks under supervision, implement decisions made by others, or hold delegated authority for pre-approved or administrative matters. The absence of final or ultimate strategic decision-making authority or binding authority means the individual does not meet the officer threshold.

Examples of Persons Who May Be Officers

CTP010 explicitly identifies the following roles as persons who may qualify as officers:

- Chief Executive Officer (CEO)

- General Manager

- Chief Financial Officer (CFO)

- Chief Operating Officer (COO)

- Chief Commercial Officer (CCO)

- An authorised representative holding discretionary authority

Critically, the legal title is not the only determining factor. A person without a formal C-suite designation who, in practice, has real authority to plan, direct, control, make strategic decisions or legally bind the business may still qualify as an officer under CTP010. This is particularly relevant to SMEs where formal governance structures may not accurately reflect actual decision-making authority.

Which Payments Are Subject to Connected Person Rules?

The Connected Person rules can apply to a wide range of payments and benefits, including:

- salaries paid to owner-managers;

- director fees and board remuneration;

- bonuses and performance incentives;

- housing, schooling, car, travel or other personal allowances;

- management fees paid to owners or family members;

- consultancy fees paid to a shareholder or a shareholder’s relative;

- benefits in kind;

- rent or service charges paid to a Connected Person;

- payments to an outsourced manager or secondee who holds strategic authority; and

- payments to a person holding a power of attorney where that authority is substantive.

The tax issue is not whether these payments are commercially reasonable in principle. The Corporate Tax question is whether the amount is deductible for Corporate Tax purposes and whether it must be disclosed in the Tax Return.

The Primary Tax Risk: Excessive or Unsupported Deductions

Consider a UAE company paying an owner-manager AED 900,000 per year. That payment is not automatically disallowed. It may be fully deductible if the person genuinely performs services for the company, the amount reflects Market Value and the expense is wholly and exclusively incurred for the purposes of the business.

However, if the company cannot support the amount, or if the amount exceeds what independent parties would reasonably pay for comparable services in comparable circumstances, the excess may be disallowed under the Connected Person rules.

The practical result is an increase in the company’s Taxable Income and additional Corporate Tax exposure.

Salary vs. Dividends: What Owner-Managed Businesses Need to Know

One of the most common questions for owner-managed businesses is whether the owner should receive salary, dividends or a combination of both.

The answer turns on the legal form and the substance of each payment:

- A salary or management fee is ordinarily intended to compensate a person for work performed. For Corporate Tax purposes, it must be supported by actual services, proper documentation and Market Value.

- A dividend or profit distribution is a return on ownership. It is not a deductible business expense of the paying company.

The company should not classify a profit distribution as salary simply to generate a tax deduction. Equally, a genuine salary paid for genuine services should not be recharacterised as a dividend because the recipient is also a shareholder. The classification must follow the legal form, accounting treatment and commercial substance of the arrangement.

Why Connected Person Rules Matter More for SMEs

The Connected Person rules have particular relevance for small and medium-sized enterprises because many SMEs are managed informally and documentation practices may not have kept pace with the UAE’s Corporate Tax framework.

Common issues that can create Connected Person risk in SME environments include:

- owners receiving monthly amounts without a formal employment or service agreement;

- family members on payroll without clearly defined roles or time records;

- year-end bonuses approved without a documented bonus policy;

- personal expenses recorded as business costs;

- company cars, travel or accommodation used partly for personal purposes;

- shareholder withdrawals treated inconsistently as salary, loan, dividend or expense; and

- management fees paid without invoices, deliverables or evidence of services rendered.

These practices may not have created significant tax exposure before the introduction of UAE Corporate Tax. They now directly affect the Corporate Tax Return, which begins from accounting profit and applies tax adjustments, including specific adjustments for Related Party and Connected Person transactions as part of the Taxable Income calculation.

Disclosure in the Corporate Tax Return

Article 55(1) of the UAE Corporate Tax Law permits the FTA to require a Taxable Person to file a disclosure, together with its Tax Return, containing information on transactions and arrangements with Related Parties and Connected Persons.

CTP010 confirms that the FTA currently requires payments or benefits provided to Connected Persons to be disclosed in the Tax Return where they exceed a specified threshold.

The precise reporting requirements should be verified against the Corporate Tax Return and the FTA’s current filing guidance at the time of submission. The key practical point is this: businesses should identify Connected Person payments and prepare the disclosure well before filing, not during the submission process.

Transfer Pricing Under the UAE Corporate Tax Connected Person Rules

Transfer pricing is not exclusively a concern for large multinational groups. The FTA General Corporate Tax Guide confirms that transfer pricing rules apply to transactions between Related Parties and Connected Persons, including both cross-border and domestic transactions carried out by juridical persons and individuals.

For SMEs, this does not necessarily mean a full benchmarking study is required for every transaction. The appropriate level of documentation is proportionate to the size, complexity and risk of the transaction.

That said, businesses should maintain reasonable evidence showing:

- who was paid;

- why the payment was made;

- what service, benefit or value was received;

- how the amount was determined;

- why the amount is commercially reasonable; and

- whether the arrangement is consistent with independent-party behaviour.

For significant owner salaries, director fees, bonuses or management charges, a more formal remuneration review or benchmarking analysis may be appropriate and proportionate.

Does Small Business Relief Remove These Obligations?

Businesses that qualify for Small Business Relief may elect to be treated as having no Taxable Income for the relevant Tax Period, subject to meeting the applicable conditions. The Small Business Relief Guide provides that the relief applies where Revenue does not exceed AED 3 million in the relevant Tax Period and in all previous Tax Periods ending on or before 31 December 2026, and where the election is made in the Tax Return.

Where Small Business Relief applies, Article 21 of the Corporate Tax Law provides that certain provisions, including deduction rules and Article 55 disclosure requirements, do not apply for that Tax Period.

However, qualifying for Small Business Relief does not remove the need for discipline in relation to Connected Person arrangements. There are three practical reasons:

- The business may not qualify for Small Business Relief in a future Tax Period.

- The relief is time-limited to Tax Periods ending on or before 31 December 2026, subject to the law and applicable conditions.

- The FTA can still review eligibility, Revenue records and potential artificial separation of business activities.

The Small Business Relief Guide explicitly warns that artificial separation of a business designed to remain below the AED 3 million threshold may be challenged under the General Anti-Abuse Rule.

Practical Examples: CTP010 Applied

1. Founder-Manager Salary

A shareholder works full-time as CEO and receives a monthly salary. The salary may be deductible where it reflects the work performed, is properly documented and does not exceed Market Value. Supporting documentation should include an employment agreement, job description, payroll records, board approval and market support for the compensation level.

2. Family Member on Payroll

A spouse or child of an owner is employed and paid by the company. The payment is not automatically disallowed, but the company must demonstrate that the individual genuinely works for the business, has a defined role and is remunerated at a commercially reasonable level.

3. “Director” Title Without Board Appointment

A person holds the title “Operations Director” but has not been appointed to the board or an equivalent governing body. Under CTP010, the title alone does not constitute a directorship under Article 36. However, the individual may still qualify as an officer if they hold final strategic authority or binding authority over the business.

4. General Manager with Authority

A General Manager who holds authority and responsibility for the overall management of an LLC may qualify as an officer. Payments to that person may therefore fall within the Connected Person rules where the relevant conditions are met. CTP010 cites this as a directly relevant example.

5. Power of Attorney Holder

An employee holding a power of attorney may qualify as an officer if the power of attorney grants discretionary authority to plan, direct and control activities, make final strategic decisions or legally bind the company. Where the power of attorney is limited to administrative or pre-approved tasks, the person may not meet the officer threshold.

6. Interim CEO or Outsourced Management

A person engaged as a consultant or outsourced manager may still qualify as an officer if they perform the substantive functions of a CEO or hold final authority over the business. CTP010 confirms that substance matters more than the label used in the engagement contract.

What Good Documentation Looks Like

A defensible Connected Person file should contain the following, as applicable:

- a Related Party and Connected Person register;

- ownership structure and family relationship mapping;

- board resolutions or shareholder approvals;

- employment contracts, director appointment letters or consultancy agreements;

- job descriptions and an authority matrix;

- payroll records, WPS confirmation and payment records;

- a documented bonus policy and performance criteria;

- evidence of work performed;

- market salary or fee benchmarking support;

- benefit policy and valuation support for benefits in kind;

- invoices, deliverables and service records for management or consultancy fees;

- accounting treatment and tax adjustment working papers; and

- Corporate Tax Return disclosure support documentation.

The objective is not simply to complete the Tax Return. The objective is to make the company’s position understandable and defensible in the event that the FTA queries why a particular payment was treated as deductible.

Common Mistakes to Avoid

Owner-managed businesses should be alert to the following:

- treating all owner withdrawals as deductible salary without classification;

- paying family members without defined roles, agreements or time records;

- recording private expenses as business expenses;

- relying on job titles without assessing actual decision-making authority;

- assuming a shareholder salary is automatically deductible in full;

- assuming director fees are automatically deductible without support;

- failing to separate salary, loan, dividend and expense accounts;

- approving large year-end bonuses without a policy, minutes or evidence;

- overlooking Connected Person disclosure requirements in the Tax Return; and

- beginning the Corporate Tax Return without first reviewing Related Party and Connected Person transactions.

Key Takeaway

CTP010 is a valuable reminder that UAE Corporate Tax is not only a matter of calculating profit and applying a 9% rate. For owner-managed businesses, the real compliance risk often lies in the detail: who was paid, why they were paid, how much they were paid, and whether the company can demonstrate that the payment reflects Market Value.

Under the UAE Corporate Tax Connected Person rules, Connected Person payments can be legitimate and deductible, but only to the extent they reflect Market Value, are incurred for the business, and are properly structured, approved, recorded and supported.

For UAE SMEs, the most prudent approach is to review owner salaries, director fees, management charges, family payroll, bonuses and benefits before filing the Corporate Tax Return, not after the FTA raises questions.

How Audiix Can Help

Audiix supports UAE SMEs, owner-managed businesses and foreign-owned entities in reviewing Connected Person and Related Party transactions before Corporate Tax filing — as part of Corporate Tax compliance, Transfer Pricing support, or ongoing accounting and tax advisory.

Audiix can help you review owner payments, related-party transactions and supporting documentation early, so your Corporate Tax position is properly recorded, commercially supported and ready when filing time comes.