Many individuals in the UAE ask how UAE Corporate Tax on real estate income applies when they own property personally, rent out apartments, villas, warehouses, offices, holiday homes, or commercial units, or buy and sell property as part of their personal investment portfolio.

A common question arises:

“Do individuals pay UAE Corporate Tax on rental income or gains from selling property?”

The short answer is: not always.

Under the UAE Corporate Tax rules, qualifying Real Estate Investment income earned by a natural person is excluded from Corporate Tax, provided the specific conditions are met. The key issue is not whether the income comes from property, it is whether the real estate activity is conducted, or required to be conducted, through a Licence from a UAE Licensing Authority.

This distinction matters in practice. A passive landlord may be outside Corporate Tax. A licensed holiday home operator may be within Corporate Tax. A person using a third-party property manager may still be outside Corporate Tax, while a person using a licensed sole establishment for property leasing or management may not be.

This article explains the UAE Corporate Tax treatment of real estate income for natural persons, based on the UAE Corporate Tax Law, Cabinet Decision No. 49 of 2023, and the FTA’s Corporate Tax Guide on Real Estate Investment for Natural Persons.

1. Quick Answer: Is UAE Corporate Tax on Real Estate Income Payable by Individuals?

For a natural person, income from Real Estate Investment is generally not subject to UAE Corporate Tax where it qualifies for the Real Estate Investment exclusion.

Under Article 1(1) of Cabinet Decision No. 49 of 2023, Real Estate Investment means any investment activity conducted by a natural person, directly or indirectly, in relation to the sale, leasing, sub-leasing, or renting of land or real estate property in the UAE, provided the activity is not conducted, and does not require to be conducted, through a Licence from a Licensing Authority.

In practical terms:

- If an individual personally owns a property and rents it out without needing a business licence, that income may be outside UAE Corporate Tax.

- If an individual sells a personal property and no licence is required for the sale, any gain may fall within the Real Estate Investment exclusion.

- If an individual rents out property as a licensed holiday home business, that income may be taxable if the AED 1 million Turnover threshold is exceeded.

- If an individual uses a third-party property management company as agent, the individual’s rental income may still qualify as Real Estate Investment income.

- If an individual operates through a licensed sole establishment or sole proprietorship for property leasing or management, the income may fall within Corporate Tax.

The amount of rent, the number of properties, and the value of the real estate are not, by themselves, decisive. The critical question is whether the activity satisfies the definition of Real Estate Investment and whether it is conducted, or required to be conducted, through a Licence.

2. How UAE Corporate Tax Applies to Natural Persons

A natural person is an individual human being, distinct from a juridical person such as an LLC, free zone company, foundation, or other entity with separate legal personality.

Under the UAE Corporate Tax rules, natural persons are only subject to Corporate Tax on Business or Business Activities conducted in the UAE where the total Turnover from such Business or Business Activities exceeds AED 1 million within a Gregorian calendar year.

Legal reference: Article 11(6) of Federal Decree-Law No. 47 of 2022, read with Article 2(1) of Cabinet Decision No. 49 of 2023.

The following income categories are not treated as arising from Business or Business Activity and are disregarded when determining the AED 1 million Turnover threshold:

- Wage;

- Personal Investment income; and

- Real Estate Investment income.

Legal reference: Article 2(2) of Cabinet Decision No. 49 of 2023.

This means an individual could receive substantial rental income and still not be required to register for UAE Corporate Tax, provided the income properly qualifies as Real Estate Investment income and the individual has no other taxable Business or Business Activity Turnover exceeding AED 1 million.

However, where an individual conducts a taxable Business or Business Activity in the UAE and the AED 1 million Turnover threshold is exceeded, Corporate Tax registration, record-keeping, filing, and payment obligations may apply.

3. What Counts as Real Estate Investment Income?

Real Estate Investment income is income from utilising the land or real estate property itself, not from providing services connected to property. This distinction is central to the Corporate Tax analysis.

Under Article 1(1) of Cabinet Decision No. 49 of 2023, Real Estate Investment for natural persons covers investment activity relating directly or indirectly to:

- sale of land or real estate property;

- leasing;

- renting; or

- sub-leasing.

Examples of income that may qualify:

- Rental income from leasing an apartment.

- Rental income from leasing a commercial unit.

- A gain from selling a personally owned property.

Examples of income that do not qualify:

- Property management fees earned for managing someone else’s property, this is service income and may be taxable Business income.

Many property-related activities look similar commercially but are treated differently for Corporate Tax purposes. Owning and renting out your own property is not the same as operating a property management business.

4. What Types of Property Can Qualify?

The Real Estate Investment exclusion is not limited to residential property. For this purpose, real estate may include:

- land;

- buildings;

- structures or engineering works permanently attached to land;

- fixtures or equipment that form a permanent part of the land or building;

- residential properties;

- furnished holiday homes;

- commercial properties;

- showrooms;

- warehouses;

- storage rooms;

- parking lots;

- garages;

- agricultural land;

- industrial land; and

- residential land.

The tenant’s use of the property is not, by itself, decisive. For example, if an individual owns a commercial building and leases it to a company for a fixed annual rent, the income can still qualify as Real Estate Investment income, provided the individual is not required to hold a Licence for that leasing activity.

5. The Licence Test: The Decisive Factor

The most important test is whether the activity is conducted, or required to be conducted, through a Licence from a Licensing Authority.

A Licensing Authority is an authority in the UAE responsible for licensing or authorising the conduct of a Business or Business Activity. Depending on the Emirate and activity, this may include Departments of Economic Development, tourism authorities, land departments, municipalities, and free zone authorities.

A Licence is a document issued by a Licensing Authority that authorises or permits a Business or Business Activity to be conducted in the UAE. This is a broad concept, it is not limited to a traditional trade licence. The FTA confirms that a document issued by the Dubai Department of Economy and Tourism allowing a natural person to lease holiday homes would constitute a relevant Licence for this purpose.

By contrast, administrative tenancy registrations such as Ejari in Dubai or Tawtheeq in Abu Dhabi are not treated as Licences. They are tenancy registration records, not permission to conduct a Business.

Three key points follow from this:

- Ejari or Tawtheeq registration for a normal tenancy does not mean the individual is conducting a licensed Business.

- A holiday home permit or similar authorisation may indicate that the activity is conducted through a Licence.

- If a Licence is legally required but the individual does not obtain it, the absence of the Licence does not take the activity outside Corporate Tax.

If the activity is required to be conducted through a Licence, it may be treated as a Business or Business Activity within the scope of Corporate Tax, subject to the AED 1 million Turnover threshold.

6. Real Estate Income That May Be Outside Corporate Tax

The following types of income may generally fall outside Corporate Tax for a natural person, subject to the facts and licensing position:

1. Long-term residential rent

An individual owns an apartment and leases it under a normal tenancy contract without holding, or being required to hold, a Licence. This may qualify as Real Estate Investment income.

2. Commercial property rent

An individual owns a warehouse, office, or showroom and leases it to a company. The individual is not involved in the tenant’s business and does not require a Licence for the leasing activity. This may qualify as Real Estate Investment income, even if the tenant uses the property for Business.

3. Variable rent linked to tenant performance

An individual leases a property to a commercial tenant and receives rent calculated partly by reference to the tenant’s revenue. If the individual is not involved in the tenant’s business and does not require a Licence, the rental income may still qualify as Real Estate Investment income.

4. Sale of personally owned property

An individual sells personally owned real estate at a gain without requiring a Licence. The gain may qualify as Real Estate Investment income.

5. Rental income received through a third-party agent

Using a licensed real estate agent or property management company does not automatically make the individual’s rental income taxable.

If the individual remains the owner, landlord, or lessor, the tenancy agreements name the individual as landlord or owner, and the property manager acts only as agent or service provider, the rental income may remain Real Estate Investment income of the individual.

The property manager’s Licence does not automatically become the individual’s Licence. However, the arrangements should be reviewed carefully. If the property management company is not merely acting as agent, but is the principal under the tenancy arrangements or has the right to use and sublease the property, the tax analysis may change.

Practical documents to review include the title deed, tenancy contracts, property management agreement, rent collection records, bank statements, and any related-party arrangements if the manager is connected to the individual.

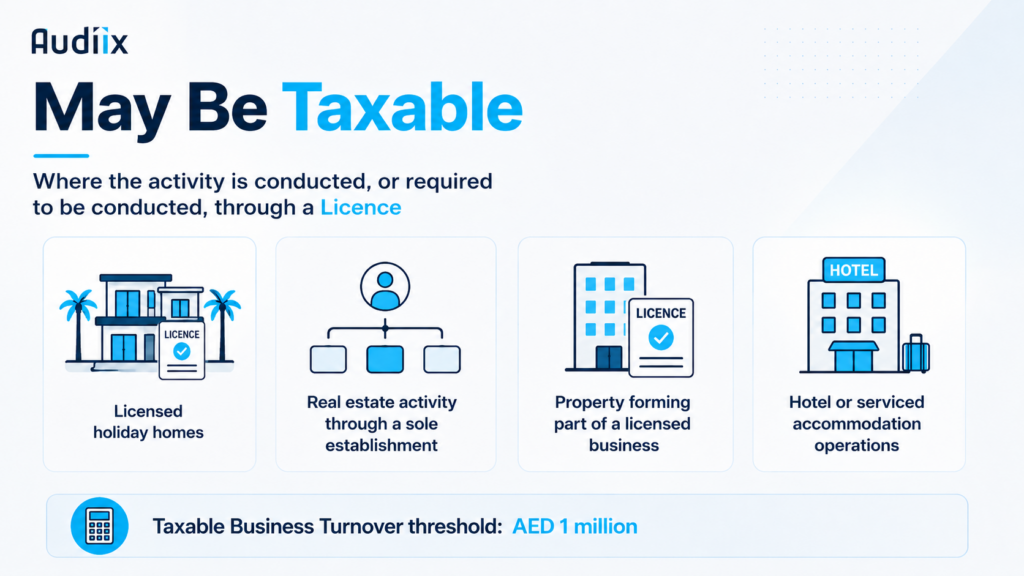

7. When Real Estate Income May Become Taxable

Real estate income may fall within the scope of UAE Corporate Tax where the relevant activity is conducted, or required to be conducted, through a Licence.

1. Licensed holiday home activity

Holiday home activity is one of the clearest examples of real estate income that can move from passive investment income into taxable Business income.

If an individual rents out properties as holiday homes and obtains permits or licences from the relevant authority, the activity may be treated as a Business or Business Activity conducted through a Licence.

In that case, the income from the licensed holiday home activity may be included in the individual’s taxable Business Turnover. If the AED 1 million Turnover threshold is exceeded in the Gregorian calendar year, Corporate Tax registration may be required, and filing obligations may apply.

The same individual may still own other apartments rented under normal residential tenancy contracts, not covered by holiday home permits and not requiring a Licence. The income from those apartments may qualify as Real Estate Investment income. This means one individual can have both taxable holiday home income and excluded Real Estate Investment income, which must be separated clearly.

2. Real estate activity through a licensed sole establishment

A sole establishment or sole proprietorship is not legally separate from the natural person for Corporate Tax purposes. The individual and the sole establishment are treated as one and the same Person.

This means that if an individual owns real estate personally but operates a licensed sole establishment for property management, leasing, or dealing in real estate, the activity may be treated as conducted by the individual through a Licence. In that case, the Real Estate Investment exclusion may not apply.

This is one of the most significant practical risks for individual property owners. A company, by contrast, has separate legal personality. If a company owns the property and earns the rent, the company’s Corporate Tax position is assessed separately from the shareholder’s personal tax position.

3. Property forming part of a licensed business

If land or real estate property forms part of an individual’s licensed Business or Business Activity, income from that property may not qualify as Real Estate Investment income.

For example, if the property is used as part of the licensed business, or the income is connected with that business, the exclusion may not apply.

4. Hotel or serviced accommodation operations

If an individual merely leases a building to a licensed hotel management company without involvement in the hotel operations, the rent may qualify as Real Estate Investment income.

However, if the individual personally operates the hotel or accommodation business and that activity requires a Licence, the income may fall within Corporate Tax.

8. Mixed Income Streams: Separating Taxable and Excluded Real Estate Income

Many individuals have mixed income streams. Each must be analysed separately.

For example, an individual may:

- operate a licensed business;

- own residential apartments personally;

- hold commercial property personally;

- rent some units as holiday homes;

- use a third-party property manager;

- own shares in a UAE company that owns real estate; and

- enter into leases with related parties.

| Scenario | Likely Corporate Tax Treatment |

| Individual rents personally owned residential apartment, no Licence required | Usually outside Corporate Tax as Real Estate Investment income |

| Individual rents commercial unit to a company, no Licence required | Usually outside Corporate Tax as Real Estate Investment income |

| Individual rents holiday homes under permits/licence | Potentially taxable Business income |

| Individual uses third-party property manager as agent | May remain Real Estate Investment income of the individual |

| Individual uses own licensed sole establishment for property leasing or management | Potentially taxable Business income |

| Individual owns shares in a UAE company that owns real estate | Company assessed separately; dividends to individual may be Personal Investment income |

| Individual leases property to a related company | Analyse Real Estate Investment exclusion and arm’s length terms |

| Individual has both licensed and non-licensed property activities | Split income and expenses between taxable and excluded activities |

Avoid treating all property income as a single category. UAE Corporate Tax requires classification based on the legal owner, licensing position, activity, contracts, accounting treatment, and related-party arrangements.

9. Expense Treatment and Apportionment

If Real Estate Investment income is excluded from Corporate Tax, the related expenses are also outside the Corporate Tax calculation.

This means expenses linked to excluded rental or property income cannot be deducted against taxable Business income, and any losses from excluded Real Estate Investment cannot be used for Corporate Tax relief.

Where expenses relate to both taxable and excluded activities, they should be allocated using a fair, reasonable, and consistent method, such as property value, floor area, usage, number of units, or another measurable basis.

The principle is straightforward: a natural person cannot exclude real estate income from Corporate Tax while deducting the related costs against taxable Business income.

10. Jointly Owned Property and Family-Owned Real Estate

Where land or real estate property is jointly owned, income must be allocated to each owner, who must then assess their own Corporate Tax position separately.

Different owners may have different outcomes. One co-owner may conduct a licensed real estate business; another may hold property purely passively. Some properties may be rented as holiday homes; others under normal residential tenancy contracts. The ownership percentage will also affect each owner’s Turnover calculation.

Where an owner is a natural person, their allocated income may be outside Corporate Tax if they do not conduct the Real Estate Investment activity through a Licence and are not required to do so.

11. Record-Keeping: What Individual Property Owners Should Document

Even where real estate income is outside UAE Corporate Tax, individuals should keep records to support the treatment. The key records include:

- ownership documents, such as title deeds;

- tenancy contracts and tenancy registrations, such as Ejari or Tawtheeq;

- holiday home or tourism permits, if applicable;

- property management agreements and agent invoices;

- rent collection records and bank statements;

- expense invoices and allocation workings for mixed activities;

- related-party agreements and market rent support, where relevant; and

- Corporate Tax registration, filing, and accounting records, if applicable.

The objective is simple: the individual should be able to demonstrate why the income was treated as excluded Real Estate Investment income.

Do You Need to Register for UAE Corporate Tax?

Use this step-by-step checklist:

Step 1: Are you a natural person?

These rules apply to individuals, not companies or other juridical persons. If the property is owned by a company, that company’s Corporate Tax position is assessed separately.

Step 2: Is the income from selling, leasing, renting, or sub-leasing land or real estate property?

If yes, the income may qualify as Real Estate Investment income.

Step 3: Is the activity conducted, or required to be conducted, through a Licence?

This is the key test. If no Licence is held or required, the income is generally outside Corporate Tax. If a Licence is held or legally required, for example, for certain holiday home or licensed real estate activities, the income may fall within Corporate Tax.

Step 4: Is the property income separate from any licensed business activity?

The income streams should be separated clearly. An individual may operate a licensed business but still earn qualifying rental income from personally held apartments outside that business.

Step 5: Does taxable Business Turnover exceed AED 1 million in the Gregorian calendar year?

A natural person must register for Corporate Tax only where total Turnover from Business or Business Activities conducted in the UAE exceeds AED 1 million in a Gregorian calendar year. Real Estate Investment income that qualifies for the exclusion is not counted towards this threshold.

In summary: an individual who earns only qualifying rental income from personally held property may not need to register for Corporate Tax, even if that rental income exceeds AED 1 million. However, if the individual earns more than AED 1 million from taxable Business or licensed real estate activities, Corporate Tax registration may be required.

Where the position is mixed, for example, licensed holiday home income combined with non-licensed residential rental income, the taxable and excluded income must be separately tracked, supported, and documented.

If an individual has more than one taxable Business or Business Activity in the UAE, the Turnover from those activities should be combined for the AED 1 million threshold. This can include income earned personally, through a sole establishment, or from real estate activity that does not qualify for the Real Estate Investment exclusion because it is conducted, or required to be conducted, through a Licence.

Therefore, even if the taxable real estate activity is below AED 1 million on its own, Corporate Tax registration may still be required if, together with the individual’s other taxable Business Turnover, the total exceeds AED 1 million in the Gregorian calendar year.

How Audiix Can Help

Audiix can help individual property owners, founders, investors, and family property owners assess whether their real estate income is outside UAE Corporate Tax or should be treated as taxable Business income.

We can review your ownership structure, licences, tenancy contracts, property management arrangements, and related records before you register, file, restructure, or rely on the Real Estate Investment exclusion.

Conclusion

UAE Corporate Tax on real estate income for individuals is not automatic: real estate income may be outside Corporate Tax, but it is not automatically excluded either.

For natural persons, qualifying Real Estate Investment income may be outside Corporate Tax where it relates to the sale, leasing, renting, or sub-leasing of land or real estate property, and the activity is not conducted, or required to be conducted, through a Licence.

The licence test is the decisive factor. Qualifying passive rental income may be outside Corporate Tax where the activity is not conducted, and is not required to be conducted, through a Licence. Licensed holiday home activity, or real estate activity through a licensed sole establishment, may be taxable.

The safest approach is to review the ownership structure, licensing position, contracts, income flows, expense allocation, and supporting records before any registration or filing deadline.